CNHO – A Decentralized Offshore China Yuan RMB Stablecoin

1. Introduction

Stablecoins serve as a bridge between blockchain networks and the real-world economy. They play a pivotal role in the crypto asset ecosystem—not only as units of account and trading pairs, but also as core instruments for value storage, payment settlement, and price stability.

At present, the global stablecoin market is overwhelmingly dominated by the U.S. dollar. USDT and USDC together account for over $120 billion in market capitalization, making up more than 90% of the entire stablecoin sector. This monopolistic reliance on a single currency framework ties the blockchain economy tightly to U.S. monetary policy and regulatory risks. For regions and communities seeking diverse financial sovereignty, this poses a significant and growing concern.

It is within this context that CNHO (Offshore China Yuan) was born.

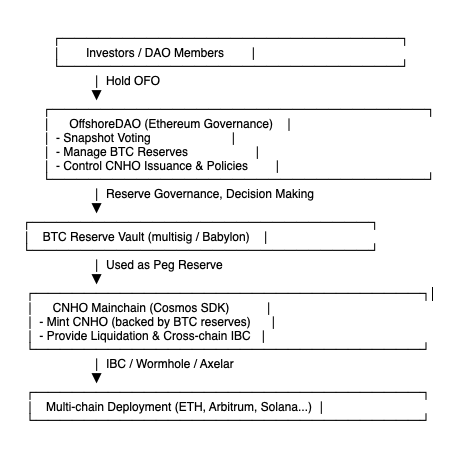

CNHO is a decentralized stablecoin pegged 1:1 to the offshore renminbi (CNH). It is designed to offer a regional crypto asset alternative—one that does not rely on the U.S. dollar, centralized custodians, or government backing. CNHO is issued and governed by OffshoreDAO, and is entirely built on blockchain-native technologies and community-driven governance. Its price stability is maintained through multi-asset on-chain collateralization and supported by decentralized oracle feeds.

The offshore RMB (CNH) has been active in global markets for over a decade. It offers higher liquidity, transparency, and freedom of movement compared to the onshore RMB (CNY), which remains under the control of the People’s Bank of China. CNH is actively used in financial centers such as Hong Kong, Singapore, and London. CNHO combines CNH’s global liquidity with the decentralized nature of blockchain technology, creating a trustless cryptographic version of CNH designed to serve users and developers across the Asia-Pacific region.

CNHO Use Cases:

- Unit of account for regional DeFi: Provides a familiar, stable, and non-USD alternative for Asia-Pacific protocols and users.

- Stable income tool for Web3 developers and creators: Enables DAOs and open-source communities to pay contributors in CNH terms.

- Cross-border settlement channel for SMEs: Especially useful in Southeast Asia and Greater China trade contexts.

- Collateral and liquidation unit for on-chain leveraged assets: A CNH-denominated standard for DeFi lending and risk management.

Beyond being a stablecoin, CNHO is also a community-led experiment in monetary governance. While traditional currency policies are determined by sovereign states via central banks, CNHO’s monetary parameters—including collateral ratios, liquidation rules, oracle configuration, bridge strategies, and supply controls—are all decided by holders of the $OFO governance token via OffshoreDAO.

This means CNHO is not controlled by any single company or development team. It is collectively owned and governed by its participants. Such an open governance structure promises to build a more resilient, transparent, and community-aligned financial system.

We believe that the internationalization of the renminbi is not solely a state-led monetary strategy—it can also be a decentralized experiment in technology and trust, led by a global Web3-native community.

CNHO is not a replication of central bank functions. Rather, it is a complementary alternative: a decentralized offshore RMB system running on cryptographic consensus and smart contract logic. It offers a new model of value stability—originating from the East, and representative of emerging regional economic aspirations.

Our goal is not to compete with USDT or USDC, but to build a stable, open value anchor for the next generation of on-chain economies—born in, built for, and understood through the context of Asia.

2. Market Background and Macroeconomic Landscape

2.1 The U.S. Dollar Monopoly in the Global Stablecoin Market

As the core infrastructure of on-chain finance, stablecoins have become increasingly critical in recent years—playing essential roles in trading, payments, lending, clearing, and asset issuance. However, the current market structure is heavily unbalanced: USD-pegged stablecoins dominate the entire ecosystem. The two major players, USDT (Tether) and USDC (Circle), together account for over 90% of the global stablecoin market by total capitalization, and they command an overwhelming share of trading volume on both decentralized and centralized exchanges.

According to Q4 2024 data, the total global stablecoin market stands at approximately $135 billion, distributed as follows:

- USDT: ~70%, backed by dollar deposits and short-term U.S. Treasury bills

- USDC: ~20%, fully collateralized by U.S. dollar assets under U.S. regulatory oversight

- Other USD-backed stablecoins (e.g., TUSD, FDUSD) comprise the remainder

By contrast, non-USD stablecoins remain extremely scarce. For example, euro-based stablecoins like EURT and yen-based stablecoins like GYEN have a combined market cap of under $500 million, accounting for less than 0.5% of the total stablecoin supply. RMB-pegged stablecoins, such as CNYT, are practically invisible in terms of liquidity and adoption.

This over-dollarization runs contrary to the decentralization and diversity that blockchain ecosystems are supposed to represent. The blockchain economy today is overexposed to a single sovereign currency, making it vulnerable to U.S. monetary policy, enforcement, and geopolitical decisions.

Moreover, most major stablecoin issuers are based in the United States, exposing them to intense regulatory pressure. Since 2023, U.S. sanctions and enforcement actions against crypto have escalated. Multiple DeFi protocols have been forced to block specific wallet addresses, and USDC has proactively frozen on-chain assets. For developers and projects operating in emerging markets, the Middle East, Southeast Asia, and beyond, such risks have become a serious point of concern.

Thus, “de-dollarization” is not just a theme in traditional geopolitics—it is becoming a critical issue in blockchain finance as well. There is an urgent need for a new class of community-governed stablecoins that reflect regional economic realities, reduce exposure to U.S. jurisdiction, and offer credible alternatives to dollar-based systems.

2.2 The Rise of the Offshore Renminbi (CNH)

The renminbi (RMB), as the monetary foundation of the world’s second-largest economy, has long entered the deep waters of internationalization. Since 2009, China has progressively built out its offshore RMB market infrastructure, forming a global clearing network based on CNH (offshore RMB).

Unlike CNY (onshore RMB), CNH is not subject to China’s capital controls, and can be freely traded and settled in major financial centers such as Hong Kong, Singapore, and London. It already operates within a mature interbank clearing and foreign exchange market.

- SWIFT data ranks RMB as the 4th most-used currency in global payments

- The IMF has included RMB in the Special Drawing Rights (SDR) basket, signaling its global reserve currency status

- In 2023, over 30% of China–ASEAN cross-border settlements were executed in CNH

- The RMB's share in trade settlements with the Middle East, Russia, and Africa is also growing rapidly

This indicates that while CNH is not yet a universal legal tender, it has already assumed a major role in real-world trade, settlement, and capital flows. CNH combines the sovereign backing of the renminbi with the flexibility and freedom of market-based operations, making it a promising candidate for on-chain value representation.

2.3 Why Blockchain Needs a CNH Stablecoin

The emergence of CNH opens new possibilities for the crypto world. Compared to the U.S. dollar, CNH offers several unique advantages that make it ideal for a blockchain-native stablecoin:

- Strong regional relevance: As a key trade settlement currency in Asia, CNH better reflects the real economic needs of East and Southeast Asia.

- Resilience against financial decoupling risks: As a non-U.S. currency, CNH provides a hedge against sanctions, blacklisting, or regulatory disruption from the U.S.

- Significant market gap: There is currently no widely adopted, community-governed CNH stablecoin with real liquidity and trust.

- Unlocks new cross-border use cases: Such as SME trade finance, localized DeFi pricing, and regional Web3 payroll and treasury operations.

In this context, CNHO is not a simple technical wrapper for CNH, but rather a new experiment in decentralized stablecoin design—rooted in CNH as a base value layer, governed by blockchain consensus, and executed through open-source and transparent architecture.

It reflects a shift toward a more multipolar, region-driven global financial order, and creates new opportunities for Asia-based users and developers to participate in, build, and shape the future of crypto-powered economies.

3. Intersection of Offshore RMB (CNH) and Blockchain

The convergence of blockchain technology and offshore renminbi (CNH) marks a pivotal opportunity to reshape cross-border finance. While digital RMB (e-CNY) is led by China's central bank with a domestic focus, CNHO represents a decentralized, market-driven counterpart that brings CNH onto blockchain rails — without relying on centralized custodians or government issuance.

3.1 Not e-CNY, Not Custodial — A Decentralized CNH Stablecoin

Unlike e-CNY, which is a centralized digital currency issued and controlled by the People’s Bank of China (PBoC), CNHO is:

- Community-governed, with no central issuer

- Backed by on-chain collateral, not bank deposits

- Freely accessible, globally and without KYC constraints

- Compliant with DeFi principles, including transparency, auditability, and censorship resistance

This makes CNHO fundamentally different from permissioned CBDCs. It is built for open blockchain ecosystems and cross-border composability — serving users and developers who seek programmable, stable value without dependency on U.S. financial rails.

3.2 Core Mechanism Design: A Trifecta of Trust

CNHO is built on a hybrid design model combining:

- 🏦 Fiat-pegged stability (CNH)

The peg to CNH reflects a real-world currency with increasing relevance in international trade, especially across Asia. - 🔐 Trust-minimized DeFi architecture

Minting and redemption of CNHO are enforced by smart contracts based on overcollateralization, automated liquidation, and decentralized governance. - 🌏 Regionally aligned economic design

CNHO is tailored for Asia-Pacific ecosystems, where CNH is already familiar to businesses, developers, and institutions.

This architecture enables CNHO to serve as more than just a stablecoin — it acts as a Web3-native representation of regional economic power.

3.3 Why CNH Makes Sense On-Chain

The choice of CNH as the anchor asset for CNHO is not arbitrary. It is based on pragmatic and strategic considerations:

- Growing cross-border relevance

CNH is already being used in settlements between China and ASEAN countries, as well as in oil trade, logistics, and manufacturing. - Reduced reliance on USD

CNH provides diversification away from dollar exposure, especially in politically sensitive or sanctioned regions. - Untapped crypto-native demand

There is a lack of credible, liquid CNH-based stablecoins in the market — representing a major opportunity for adoption. - Potential for programmable trade finance

CNHO could enable innovative products in DeFi, such as CNH-denominated yield products, synthetic trade invoices, or cross-border payroll systems.

3.4 Collateral-Backed, Not Algorithmic

CNHO is not an algorithmic stablecoin. It avoids the pitfalls of failed models like UST by anchoring its value through:

- Multi-asset overcollateralization (e.g., ETH, BTC, USDC)

- Transparent liquidation triggers

- Oracle-based real-time pricing

- DAO-controlled monetary parameters

Users mint CNHO by locking collateral in smart contracts. When collateral falls below safe thresholds, liquidation ensures solvency. All system logic is public, auditable, and governed by the OffshoreDAO, whose parameters are enforced on-chain.

3.5 More Than Just a Currency

By combining the credibility of CNH with the openness of DeFi, CNHO opens doors to multiple possibilities:

- Unit of account for Asia-centric DeFi

- Payroll for developers and DAOs in CNH terms

- Programmable cross-border trade finance tools

- Base currency for CNH-denominated RWA (real-world assets)

CNHO is not a "Chinese version of USDT." It is a decentralized, community-owned experiment in economic coordination and currency innovation.

4. Project Overview

CNHO (Offshore China Yuan) is a decentralized stablecoin pegged 1:1 to the offshore Renminbi (CNH), built on the ChainCNHO public blockchain and issued and governed by OffshoreDAO. Its design goal is to create a stablecoin that does not rely on the US dollar system, represents regional economic interests, and meets the on-chain demand for Renminbi-denominated assets in East Asia and the Global South markets.

4.1 Project Parameters

- Stablecoin Code: CNHO

- Pegged Asset: Offshore Renminbi (CNH)

- Minting Method: BTC reserve collateral

- Issuance Module: CNHO Stables native module, built on Cosmos SDK

- Issuance Governance: OffshoreDAO, controlled by governance token $OFO

- Expansion Capabilities: IBC cross-chain communication protocol, CosmWasm smart contracts, Ethereum cross-chain support

4.2 Technical Features

Native On-Chain Issuance: CNHO is not an ERC-20 token deployed on Ethereum or other general-purpose public chains. Instead, it is constructed through the ChainCNHO native module integrated into the underlying consensus mechanism and governance logic. This design is similar to TerraUSD on the Terra chain but avoids algorithmic stability, opting for on-chain collateral to ensure stability.

Multi-Asset Collateral and Risk Control Module: The collateral used to mint CNHO can include various mainstream crypto assets. In the future, governance will introduce regionally representative assets (such as HKD stablecoins and ASEAN regional tokens). The platform features a dynamic liquidation mechanism: when collateralization falls below a liquidation threshold (e.g., 150%), an automatic auction mechanism for liquidators is triggered to recover CNHO, ensuring system stability.

Governance Module: $OFO Token: OffshoreDAO adopts a token governance model with $OFO (OffshoreDAO Token) as its governance token. Holders can vote on system parameters (such as minimum collateral ratio, asset whitelist, cross-chain bridge settings) and participate in chain upgrades and community fund proposals.

Cross-Chain and Contract Expansion: The CNHO ecosystem is built on Cosmos SDK, naturally supporting IBC cross-chain protocol, enabling asset interoperability with other blockchains like Osmosis, Neutron, Injective, and more. The CosmWasm module provides smart contract functionality, enabling future applications like lending, liquidity mining, and DAO incentives. Bridges to the EVM ecosystem are also planned, expected to integrate Ethereum and Arbitrum L2 networks via protocols such as Axelar and Wormhole.

4.3 Comprehensive Positioning

CNHO is not only a stablecoin on a single blockchain but also a cross-chain composable, regionally oriented digital currency infrastructure. Compared with existing stablecoin systems dominated by the US dollar, CNHO offers a new value reference system:

- An experimental platform for de-dollarization

- An on-chain testbed for Renminbi internationalization

- An important component of Asian DeFi

In the future, CNHO will serve as the representative on-chain Renminbi stablecoin and build a Renminbi bridge to the Web3 world.

5. Stability Mechanism and Collateral Design

The core design philosophy of CNHO is to maintain a 1:1 value stability with the offshore Renminbi (CNH) under a decentralized architecture. To achieve this, CNHO employs an innovative dual-layer stability mechanism: combining fiat currency exchange with on-chain collateralized minting, paired with dynamic risk control strategies and an oracle system to balance price peg and trustless operations.

5.1 Collateralized Minting Process

The issuance process of CNHO involves both users and the DAO treasury, consisting of three main steps:

- Fiat deposit and CNHO exchange: Users deposit CNH (offshore Renminbi) through compliant entry points partnered with the DAO (e.g., OTC or third-party stablecoin gateways).

- Minting: The system mints CNHO at a 1:1 exchange rate and sends the equivalent amount to the user's on-chain address.

- Treasury reserve adjustment: The DAO treasury automatically uses the received CNH to purchase BTC or other reserve assets on secondary markets (e.g., Binance, OKX). These purchased assets enter the DAO’s decentralized reserve pool, serving as value backing for future redemptions.

5.2 Redemption Mechanism and Burn Logic

This mechanism closes the loop of “CNH deposits, BTC reserves, CNHO circulation,” ensuring the stablecoin is backed by real assets and can dynamically respond to market supply-demand and price fluctuations.

- Redemption: Users can return CNHO tokens to the contract and choose the “BTC equivalent redemption” option.

- Burn and release: The system calculates the current CNHO value based on oracle prices, burns the returned CNHO, and releases the equivalent BTC to the user’s address.

5.3 Risk Control Strategies

To guarantee CNHO’s stability and system security, OffshoreDAO has established three core risk control modules:

- Dynamic Collateral Ratio Design: The system automatically adjusts the treasury BTC reserve coverage ratio according to BTC volatility. An algorithm builds a volatility model based on the past 180 days’ average daily BTC prices, dynamically raising or lowering the minimum collateral ratio (e.g., from 150% to 200%) to prevent insolvency during price downturns and protect CNHO stability.

- Oracle Module: A dual oracle price feed system integrating Band Protocol and Chainlink self-operated nodes is used. Price data for BTC and CNHO is updated in a decentralized manner, avoiding single points of failure and data manipulation risks. If oracle prices deviate drastically, a safety module automatically triggers adjustments or pauses redemption.

- Safety Module and Emergency Mechanism: In extreme cases (such as sudden BTC crashes or on-chain attacks), the DAO can activate an “emergency freeze mechanism” to suspend new minting or redemptions. The system can set a “hard redemption ratio” — for example, if the market price crashes significantly, only 80% redemption is allowed to protect system assets from rapid depletion.

The stability mechanism employed by CNHO combines the strengths of fiat exchange and decentralized collateralization. It is not merely a USD stablecoin substitute but a crypto representation of the Renminbi tailored for the real economy in the Asia-Pacific region. Through rigorous reserve management and on-chain risk control modules, CNHO ensures stability while providing a transparent, verifiable, and censorship-resistant global stablecoin solution.

6. DAO Governance Model

OffshoreDAO is the core governance entity of the CNHO stablecoin system. Its operation mechanism is fully built on blockchain technology, realizing a decentralized, transparent, and community-participatory governance model. Through the governance token $OFO, any community member can participate in proposals, voting, and parameter decisions, driving the evolution and upgrades of CNHO.

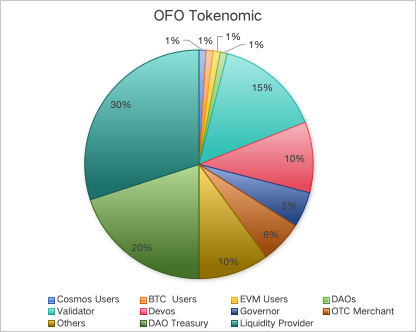

6.1 Basic Information of Governance Token

- Token Name: OffshoreDAO

- Token Symbol: OFO

- Total Supply: 1,000,000,000 tokens

- Distribution: Community Airdrop (4%), Contributors (46%), Treasury (20%), Liquidity Mining (30%)

6.2 Governance Structure and Operating Logic

The governance framework of OffshoreDAO is based on the Cosmos SDK governance module, combined with a multi-level community participation mechanism:

- Proposals and Voting: Addresses holding more than 1,000 OFO tokens can initiate proposals, including parameter changes, module upgrades, asset support adjustments, etc. All token holders can participate in voting. A proposal passes only if it meets the minimum on-chain participation and approval ratios set by the protocol.

- Modular Governance Items: Through community voting, the following key parameters can be adjusted:

- Minting collateral ratio

- Liquidation discounts and time limits

- Oracle sources and their weights

- Treasury asset rebalancing logic

- Transparent Auditing and On-Chain Records: All proposals, voting results, and participant addresses are publicly recorded on-chain and permanently stored. DAO websites and blockchain explorers allow users to review governance history, enhancing transparency and accountability.

6.3 Value Support and Participation Incentives for Governance Token

OFO is not only used for voting rights but is deeply tied to the health and development of the entire CNHO ecosystem:

- Governance participation earns voting incentives (a share of treasury revenue distributions)

- Future DAO plans include a "Staked OFO" model to encourage long-term participation

- Part of the treasury surplus will be used to buy back and burn OFO tokens, increasing scarcity

6.4 Community Governance Spirit

OffshoreDAO is more than a technical system; it is a bottom-up experiment. We believe the real driver for regional stablecoin adoption is not a single company or consortium but a group of users, developers, and builders who trust in openness, transparency, and cooperation. The stability of CNHO is governed by OFO; the value of OFO is co-created by the community.

7. Technical Architecture and Module Structure

The CNHO system is built upon the Cosmos ecosystem, employing a modular architecture design. From the Layer 1 chain-level protocol to Layer 2 applications and cross-chain layers, it achieves a highly scalable, decentralized, and compliance-compatible regional stablecoin technology stack.

7.1 Layer 1: CNHO Stables Dedicated Chain

The CNHO mainnet, codenamed ChainCNHO, is built on Cosmos SDK and optimized specifically for stablecoin applications:

- Core Protocol:

- Cosmos SDK modular framework, facilitating future upgrades and governance parameter adjustments

- Tendermint BFT consensus algorithm, providing high performance and low-latency consensus layer

- Native support for IBC (Inter-Blockchain Communication), enabling cross-chain interoperability with any Cosmos ecosystem chain

- Core Module Division:

- Minting Module: Mints CNHO based on user collateral assets

- Liquidation Module: Implements automatic liquidation and reserve rebalancing in case of under-collateralization

- Oracle Module: On-chain price feeds for CNH, BTC, ETH, etc., implemented through a dual oracle source system with Band Protocol and self-operated nodes to resist manipulation

The stability and security at this layer form the foundation of CNHO as a stablecoin.

7.2 Layer 2: Application and Cross-Chain Layer

On top of Layer 1, CNHO offers various application modules and cross-chain interfaces to connect with other blockchains and real-world assets:

- Smart Contract Support (Q3 2025): CosmWasm virtual machine module will be enabled to support diverse DeFi contracts, such as CNHO Vault, CNHO Swap, CNHO Bonds, and other native applications

- IBC Cross-Chain Interoperability: Full integration with Cosmos ecosystem chains, including Osmosis (liquidity), Injective (derivatives), Neutron (strategy automation), etc. CNHO aims to become the base currency denominated in CNH on these chains

- Ethereum Bridge Plan (Second half of 2025): Planned interoperability with Ethereum through Axelar or Wormhole bridges to extend CNHO into the ERC-20 ecosystem such as Curve, Aave, Uniswap

7.3 Centralized Trading Module and Fiat On-Ramp

In addition to on-chain modules, CNHO also provides user-friendly application layer gateways:

- Trade.CNHO.IO: Centralized order matching trading platform supporting CNHO and major crypto asset trading, serving as the price anchor and liquidity engine for the CNHO ecosystem

- Fiat.CNHO.IO Fiat Module: Enables users to subscribe CNHO or redeem CNH via fiat currencies through compliant OTC channels, bridging traditional finance and on-chain finance

7.4 Architectural Design Principles

The overall technical architecture follows three major principles:

- Modularization: Plug-and-play on-chain modules and smart contract interfaces to facilitate community governance and upgrades

- Cross-chain: Deep integration with IBC and mainstream bridging protocols to enable asset and application interoperability across chains

- Real-World Integration: Providing both on-chain and off-chain entry points to lower barriers for traditional users, realizing the practicality of “On-Chain Renminbi”

CNHO’s on-chain architecture is not just a new blockchain implementation, but a trustworthy foundation underpinning a decentralized monetary system.

8. Use Cases and Potential Market

CNHO is not just an on-chain stablecoin, but a blockchain monetary infrastructure centered around the offshore Chinese Yuan (CNH). Its application potential spans DeFi, real economy, Web3 payroll, cross-border settlements, and other diverse scenarios, aiming to bridge the Asian economy with the global crypto financial market.

8.1 DeFi Pricing: A Non-USD Stablecoin Reference

- CNHO can serve as an Asian pricing unit in DeFi, helping liquidity pools and lending protocols reconstruct their pricing systems based on CNH.

- In protocols like Osmosis, Curve, and Uniswap, CNHO can be used for cross-currency arbitrage and hedging, enhancing the pricing stability of non-USD assets.

- As a non-USD stablecoin, CNHO has the potential to become the East Asian monetary anchor in a multipolar stablecoin system.

8.2 Web3 Payroll: A Stable and Familiar Regional Salary Currency

- Developer DAOs can pay salaries directly in CNHO, avoiding USD exchange and volatility risks.

- For Chinese-speaking talents outside Mainland China (e.g., Hong Kong, Taiwan, Malaysia), CNHO complements the physical RMB financial system, lowering trust and learning barriers.

- It can integrate with DAO tools like Utopia Labs, Superfluid, and Gnosis Safe for regular salary disbursement and expenditure transparency.

8.3 Cross-Border Payments: A New Option for SMEs

- Particularly suitable for medium-sized businesses engaged in trade between China and Hong Kong, supply chains in Singapore and Malaysia, and the tourism industry in Thailand requiring CNH settlements.

- Integrated with the centralized platform trade.cnho.io for fast deposits, withdrawals, and on-chain reconciliation.

- Bypassing SWIFT, reducing banking fees and time costs, creating a regional "commercial stablecoin."

8.4 Physical Link: CNHO ↔ HKD Clearing Network

- Cooperating with licensed money service providers to facilitate off-chain clearing between HKD and CNHO.

- Integrating payment tools such as FPS, PayMe, and Faster Payment System to extend to retail users.

- CNHO can flexibly move between corporate wallets, DAO treasuries, and Web3 platforms, enabling globalized funds with local compliance.

8.5 Central Bank Sandbox: A Technical Experiment for CNH Internationalization

- Acts as an experimental platform before e-CNY goes global, validating user adoption, liquidity management, and compliance models.

- Collaborates with HKEX and financial regulators to test RWA clearing, pricing systems, and liquidity risk control tools.

- In the future, CNHO may complement or support CBDCs issued by central banks.

8.6 RWA: An On-Chain Gateway to Chinese Assets

- Standardizing Chinese stocks (A-shares, H-shares), government bonds, funds, and other products as on-chain assets, enabling cross-border investments without QFII or foreign quota restrictions.

- Global holders can participate in Chinese asset trading priced in CNHO, opening new capital flow mechanisms.

- Combined with STO (Security Token Offering) frameworks cooperating with HKEX, CNHO opens a Web3 channel to Chinese capital markets.

CNHO’s potential market is not limited to crypto users but extends to the broader Pan-Chinese economic zone and global individuals and institutions interested in Chinese assets.

9. CNHO Stablecoin Economic Model

The economic model of the CNHO stablecoin is centered on zero inflation. Node revenues come entirely from transaction fees paid by users, with no need for additional token issuance subsidies. OffshoreDAO dynamically adjusts the total supply of CNHO based on actual market demand for the stablecoin, ensuring stable operation and sustainable development of the system. Adjustments to the total supply parameters are collectively voted on by $OFO holders.

9.1 On-Chain Processing Capacity and Annual Transaction Estimates

| Block Time | 5 seconds per block |

| Annual Number of Blocks | ≈ 6,307,200 blocks |

| Block Capacity | 1 MB (1,000,000 Bytes) |

| Average Transaction Size | 500 Bytes |

| Max Transactions per Block | ≈ 2,000 transactions |

| Max Annual Transactions | ≈ 1,261,440,000 transactions |

9.2 Annual Revenue Estimate (0.1 CNHO per transaction fee)

| Single Transaction Fee | 0.1 CNHO |

| Annual Total Fee Income | 126,144,000 CNHO |

| Assumed Exchange Rate | 1 CNHO ≈ 0.14 USD |

| Annual Revenue (USD) | ≈ 17,660,160 USD |

9.3 Annual Yield (Based on Total Issuance of 2 Billion CNHO)

| Total Issuance | Annual Yield |

| 2 Billion CNHO | 6.31% annualized yield |

Note: This estimate is based solely on transaction fees and does not include potential income from liquidation profits, cross-chain fees, OTC settlements, etc.

9.4 DAO Revenue Distribution Model (Governed by OffshoreDAO)

| Purpose | Percentage | Description |

|---|---|---|

| Validator Rewards | 80% | Incentivize block production and governance participation |

| Delegator Staking Rewards | 8% | Encourage ordinary token holders to contribute to network security |

| $OFO Buyback & Burn | 12% | Establish intrinsic value and deflationary expectations for the governance token |

Even with a transaction fee estimated at only 0.1 CNHO per transaction, near-maximal block utilization can sustain an annualized yield of 6.31%. The revenue model is simple, security- and governance-oriented, has good sustainability, and holds potential for expansion into diverse revenue sources such as RWA and cross-chain fees.

10. Roadmap

OffshoreDAO and the CNHO project follow a step-by-step open and modular expansion development strategy. Since the project inception in early 2025, the testnet and basic functional modules have been completed. In the coming quarters, the project will continue to advance protocol evolution, market expansion, and governance implementation.

- 2024 Q1 – 2025 Q1: DAO Design and Product Development Phase

- March 2024: Official project launch, OffshoreDAO established, CNHO protocol design and planning begins

- December 2024: CNHO Stables testnet launched, completion of Cosmos SDK basic modules including minting, oracle, liquidation, etc.

- March 2025: Beta launch of fiat and digital asset trading module (trade.cnho.io), supporting user KYC, CNHO ↔ BTC subscription and redemption

- 2025 Q2: Mainnet Launch Phase

- Official launch of CNHO mainnet (CNHO Stables)

- Support KYC, full CNHO minting, redemption, and liquidation processes

- Launch early user airdrop program (OFO governance token)

- Support mainstream wallets (Keplr, Leap) and IBC chain integration

- Host first community governance AMA and recruit DAO members

- 2025 Q3 – 2026 Q2: Community Building Phase

- Airdrop promotions: multiple task-based airdrops, referral rewards to rapidly expand the user base

- DAO collaboration: promote DAO alliances, node incentives, and co-governance

- Branding and marketing: global content campaigns, KOL partnerships, and community matrix operations

- Builder incentives: developer grants, node operation support, and contribution rewards

- Final goal: grow OFO / CNHO holders to over 100 million within one year

- 2026 Q3: Expansion and Governance Opening

- Open CosmWasm smart contract deployment permissions, support Layer 2 application development

- Officially launch OFO governance module with on-chain proposal and voting mechanisms

- Expand IBC cross-chain connectivity to Neutron, Osmosis, and other Cosmos application platforms

- Begin exploring CNHO as a stable pricing unit in RWA and DeFi applications

- 2027 Q4: Off-Chain Settlement and Physical Cooperation Pilots

- Collaborate with fintech companies and payment providers in East Asia

- Deploy CNHO ↔ HKD off-chain clearing sandbox to verify compliance operation models

- Initiate communication and testing reports with Hong Kong, Singapore governments and regulatory bodies

- Establish Beta program for CNHO merchant acceptance

- 2028 Q1: Ethereum Cross-Chain Expansion

- Launch Ethereum cross-chain bridge (Axelar/Wormhole)

- Support CNHO on Ethereum to enter broader DeFi ecosystems

- Engage with Layer 2 platforms (e.g., Arbitrum, Base) for cross-chain deployment scenarios

- Expand stablecoin liquidity pools and DAO payroll payment applications

- 2028 Q2+: Asia Stablecoin Alliance

- Initiate the "Asia Stablecoin Alliance" regional stablecoin cooperation alliance

- Collaborate with issuers of regional stablecoins like JPY, KRW, HKD for cross-chain liquidity pools

- Promote regulated cooperation with financial institutions (sandbox, virtual banks, etc.)

- Open CNHO+HKD+RWA triangular model pilot for asset tokenization applications in East Asia

OffshoreDAO advances development in a quarterly progressive manner, from basic module initiation to cross-chain and application scenario deployment. All functional modules prioritize decentralization, security, and compliance flexibility. The launch of governance modules will further empower community-driven development, making CNHO a truly user-defined regional stablecoin protocol.

11. Join the DAO Development

OffshoreDAO is an open and decentralized community organization dedicated to the continuous development of the CNHO stablecoin protocol. We firmly believe that truly decentralized financial infrastructure should not rely on any single entity or consortium, but rather be maintained, governed, and grown collectively by global participants.

CNHO does not belong to any central authority—it belongs to every individual who is willing to contribute, use, govern, and witness its progress. If you care about financial sovereignty, believe in the value of blockchain, and hope CNH stablecoins can bring new vitality to global Chinese communities and the Asia-Pacific economy, we warmly welcome you to join OffshoreDAO and be a part of this experiment.

We welcome the following roles to join:

Developers

- Participate in Cosmos SDK module development (minting, liquidation, governance, etc.)

- Write and deploy CosmWasm smart contracts to expand Layer 2 applications

- Provide auditing, security module design, and testing support

- Submit Pull Requests on GitHub and join technical discussions in the community

Whether you're a seasoned blockchain engineer or an open-source enthusiast student, if you have technical passion, there’s a place for you.

Users

- Participate in CNHO airdrops and early testing campaigns

- Mint CNHO by collateralizing BTC and become an active protocol participant

- Provide DEX liquidity (e.g., CNHO/ATOM pool on Osmosis)

- Use CNHO for pricing, payments, or settlement in your daily life

Your usage is more than just a transaction—it's a contribution to validating and advancing the protocol’s usability.

Partners

- On-chain protocols (e.g., lending, asset issuance) are welcome to integrate CNHO as a stable collateral asset

- Web3 DAOs can use CNHO as a payroll or compensation unit in Asia

- Traditional financial institutions (e.g., family offices, funds) can explore CNHO as an on-chain alternative to CNH

- Fiat on-ramps, payment providers, and KYC service providers are encouraged to collaborate and expand compliance use cases

We believe the value of a stablecoin comes from real-world usage—partnerships are key to realizing this vision.

Governors

- Holders of the $OFO governance token can submit proposals and vote

- Help decide key parameters such as liquidation ratio, reserve logic, and oracle settings

- Join discussions on Discord and help form community consensus

- Assist the DAO in publishing updates, executing proposals, and reviewing outcomes

This is not just about holding tokens and voting—it’s an experiment in responsibility, consensus, and future infrastructure. No matter who you are, if you’re willing to participate, you can shape the future of CNHO.

OffshoreDAO has no traditional hierarchy or centralized leadership. We are a spontaneously autonomous economic body—a new kind of "on-chain collaboration model"—and at the heart of it all is open participation.

12. Compliance and Risk Disclosure

12.1 Statement & Legal Status

CNHO (Offshore China Yuan) is a decentralized blockchain-based stablecoin, designed to serve as a digital value medium pegged to the offshore Chinese Yuan (CNH). Its goal is to meet the demand for stable assets within crypto finance and the Asia-Pacific economy. CNHO is a community-driven protocol currency and does not represent or receive endorsement from any government, central bank, or statutory financial institution.

- CNHO is not issued or authorized by the People’s Bank of China and is not a blockchain version of the Digital Yuan (e-CNY).

- CNHO does not guarantee a 1:1 equivalence with CNH under all circumstances—its market price may deviate due to supply and demand fluctuations.

- All digital assets involved in this protocol are only for use within decentralized networks and do not intend to provide fiat redemption, deposit insurance, or stored value guarantees found in traditional finance, unless we are licenced by the authority when highly demanded by the DAO community.

- CNHO to fiat services in the market, say OTC, On/off ramp etc, are provided by and among the DAO members only. We do have a centralized entity to do that at present.

12.2 Risk Categories & User Responsibility

Using CNHO and any OffshoreDAO protocol module should be considered as engaging in a high-risk, high-innovation financial ecosystem. Users are expected to read the following risk categories carefully and assume full responsibility for participation.

- On-Chain Operational Risks: Collateral asset price crashes, incorrect address use, and contract upgrade changes may cause asset loss.

- Price Depegging Risks: CNHO’s market price may diverge from CNH, especially in low-liquidity conditions.

- Governance Participation Risks: Malicious proposals, voting apathy, and legal ambiguity may expose users to losses.

- Regional Compliance Risks: Stablecoin regulations vary greatly. Users must comply with local laws and immediately cease usage if prohibited.

12.3 Compliance Framework & Governance Initiatives

- All governance records are stored on-chain using Cosmos SDK and are publicly auditable.

- All smart contracts are open-sourced and audited by third-party organizations.

- OffshoreDAO welcomes collaboration with regulatory bodies and compliance partners, particularly in regions like Singapore and Hong Kong.

12.4 Disclaimer & Final Statement

By using this protocol, minting CNHO, or participating in governance, you agree to the following:

- The protocol provides no investment advice, guarantees, or legal assurances.

- Users must assume full responsibility for local law compliance, tax reporting, and legal obligations.

- No customer service, insurance, or centralized support is provided. All operations occur on-chain in a decentralized manner.

We believe open, transparent, and autonomous crypto protocols can become the foundation of new financial infrastructure—but only when built on clear responsibilities and individual risk awareness.

CNHO is a community-led stablecoin experiment—please ensure you understand the risks before participating.

12.5 Join the Community

- Telegram: https://t.me/+STykt8EXtdRhMDNl

- Discord: https://discord.com/invite/bPmhYJc5rU

- Twitter: https://twitter.com/cnho_io

- Website: https://cnho.io

- Email: [email protected]